.svg)

.png)

Key Takeaways

- Rent reporting is the process of sending your on-time rent payments to credit bureaus so they can help build your credit history — turning a bill you already pay into a credit-building tool;

- Traditional rent payments have not been included in credit files automatically, which is why specialized rent reporting services like Esusu exist today;

- A rent reporting fee is any charge connected to having your rent reported to credit bureaus, and fees may be paid by the renter or by the property owner as a resident benefit;

- Rent reporting can help many renters — especially those with a thin file or limited credit history — build credit, but no provider can guarantee a specific credit score increase.

- Esusu is a trusted, mission-driven rent reporting partner focused on transparency, access, and long-term financial health for renters and rental communities alike.

Why Rent Reporting Matters - Especially Now

In 2026, approximately 44 million U.S. renter households pay rent every month. For most, this represents their single largest monthly expense. Yet historically, these consistent monthly rent payments have done nothing to build their credit profile — a gap that has left an estimated 45 million Americans credit-invisible or un-scoreable.

This hurts millions of renters a lot. But now, government entities such as FHFA, Fannie Mae, Freddie Mac, and FHA let rent payment history count toward home loans. They announced this on April 22, 2026. Tools like Fannie Mae's Desktop Underwriter use 12 months of rent proof from bank statements. FHFA is rolling out VantageScore 4.0 right away (okayed in 2025). FHA's TOTAL Scorecard now accepts it too. This helps renters get federally backed mortgage loans by building their credit scores through their on time rent payment history.

That's why, at Esusu, our focus is helping renters turn their existing rental payment into a powerful tool for building credit and achieving their financial goals.

In this article, we’ll cover how rent reporting works, what a rent reporting fee is, the benefits of rent reporting and its limitations, how Esusu and others approach fees, and practical questions to ask before signing up for any rent reporting service.

Not all rent reporting services operate the same way, report to all the credit bureaus used by lenders, or automatically report your payments. Some may have conditions that could affect your financial wellbeing in unexpected ways. It’s important to understand these differences before enrolling in just any rent reporting service.

What Rent Reporting Is And Is Not

So, what is rent reporting? Simply put, it is the process of having your on-time rent payments (some also report late rent payments) sent to the major credit bureaus so they can be added to your credit file and potentially influence your credit score. If you are just getting started, our guide on how to build credit with no credit history breaks down other beginner-friendly ways to start building credit beyond rent reporting.

However, unlike mortgage payments or loan payments, traditional rent has not usually been reported to credit bureaus automatically. This is why dedicated rent reporting services have emerged over the past decade, bridging a longstanding divide in how creditworthiness is measured.

Why have rent reporting services emerged? Well, because renters generally cannot self-report directly to the three credit bureaus outside of a third-party platform or app. Instead, a landlord, property manager, or third-party platforms (like us) must send the data on the renters behalf.

Unfortunately, according to a recent TransUnion study, property management involvement in reporting rent payments to the credit bureaus has recently declined, even while renters continue to actively enroll in the service through independent rent reporting apps

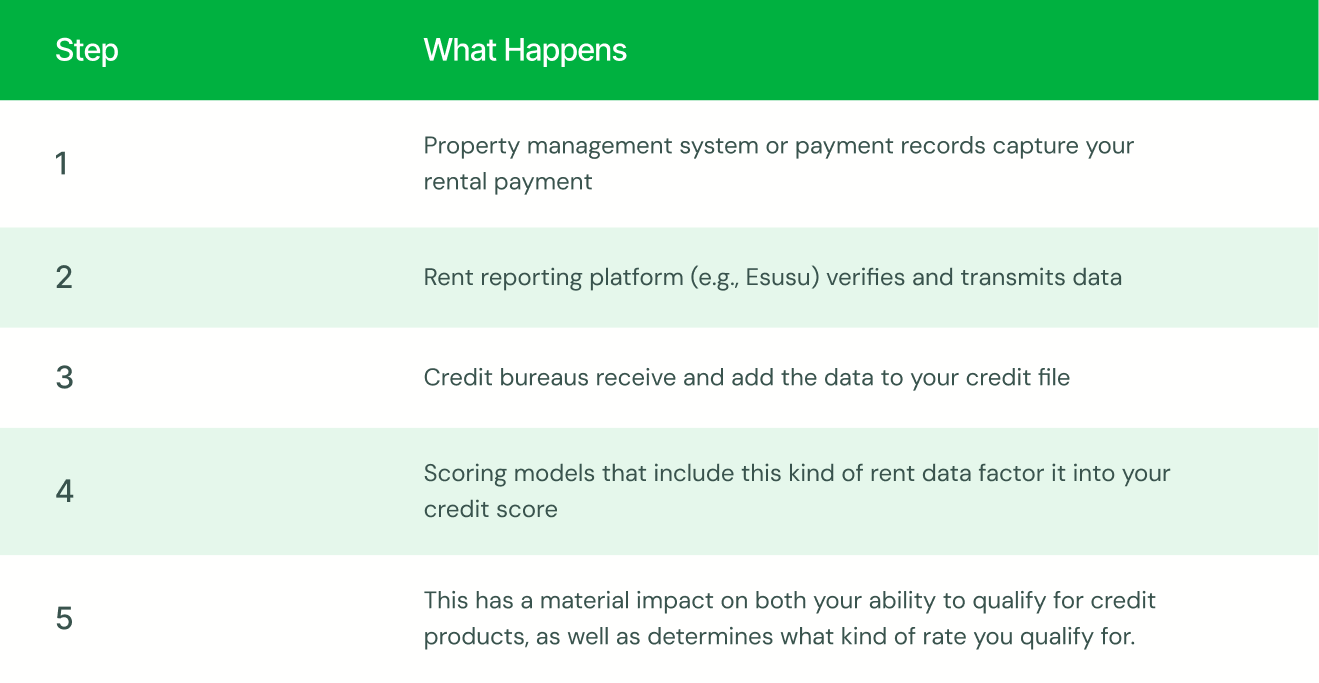

Here's what the rent reporting data flow generally looks like:

.png)

How To Report Your On-Time Rent Payments

When you participate in rent reporting, the process typically unfolds in a few clear steps.

- Get Enrolled

First, you enroll or opt in — either through a participating rental property owner, a resident portal connected to a third-party rent reporting platform, or an independent consumer app that links to your bank accounts.

- Get Verified

Next comes verification. Your identity and tenancy must be confirmed: name, address, lease dates, and monthly rent amount. This step prevents fraud and ensures your payments are accurately matched to your credit file.

- Ongoing Reporting

Ongoing reporting then begins. Each month, the platform receives your rental payment information, checks whether the payment was made on time per your current lease terms, and sends that data to one or more credit bureaus.

Policies on late or missed payments vary by provider. Some report only positive payment history (timely rent payments), while others may report late payments or a missed payment as well. Always ask explicitly what is reported before you enroll.

- Credit Score Factors

It’s important to understand: rent reporting cannot guarantee a certain credit score boost. Outcomes depend on your full credit profile, the scoring model used (such as FICO 9 or VantageScore 3.0/4.0), and the lender’s criteria. A realistic expectation is that it can take several weeks — sometimes a few months — after enrollment for a new rental tradeline to appear on your credit report and potentially influence your scores.

- Be Aware of The Dip

It's not uncommon to see a temporary dip in your credit score shortly after your first rent payment is reported, simply because it's a new tradeline. You might be able to avoid the temporary dip when you back-report up to 24 months of rent payments, rather than starting out with just one on-time rent payment being reported.

What Is a Rent Reporting Fee?

A rent reporting fee is any charge connected to having your rent payments reported to the credit bureaus, whether paid by you as the renter or by your landlord or property manager on your behalf.

Some Rent Reporting Apps Charge Additional Fees

Some rent reporting apps will charge additional fees for some rent reporting services. Those fees can add up quickly, and some are more hidden than others. Some of the fees you may see are:

- Back rent reporting for past rent payments from previous leases;

- Adding roommates or spouses to reporting;

- Premium customer support or credit monitoring features;

- Bundling utilities or other bills.

For context, while many other rent reporting services charge for it as an add-on, Esusu includes up to 24 months of prior on time rent payments as part of our services. Likewise with customer support and credit monitoring features –– those are all included with Esusu.

Fee transparency is critical. You should expect to see in writing:

- Who is being charged (renter vs. property)?

- How much and how often (monthly plan vs. annual)?

- What exactly is included (current rent, past payment history, which bureaus)?

- Are there cancellation or early-termination terms?

Compare total annual costs, not just the monthly number. And avoid services that are vague about whether they report negative marks (late or missed rent) as well as positive ones.

Limitations, Risks, and Common Misconceptions

Understanding the limits of rent reporting before enrolling is smart — especially if fees are involved.

Key limitations and risks:

- Rent reporting is not a guaranteed or instant credit score boost. Some people see noticeable improvements; others see modest change or little impact;

- Not all credit scores treat rent data the same way. Newer models like FICO 10T and VantageScore 4.0 include it, while older models (like FICO 8) may ignore it –– for now, at least;

- If a service reports late payments, those negative marks can hurt your credit. Know your provider’s policy and prioritize on-time payments;

Some services charge relatively high fees for limited benefit — especially if they report rent to only one bureau or don’t clearly describe how often they update data.

Verify before you sign up:

- Which three major bureaus does the service report to?

- How long before payments are reported to credit bureaus?

- Does reporting continue if you move to a new address?

A Common Misconception

Can landlords access your full credit score if you enable rent reporting? No, rent reporting does not give landlord reports direct access to your full credit score. Instead, it sends payment data to independent credit bureaus, which lenders and housing providers may later review through standard credit check, or tenant screening processes.

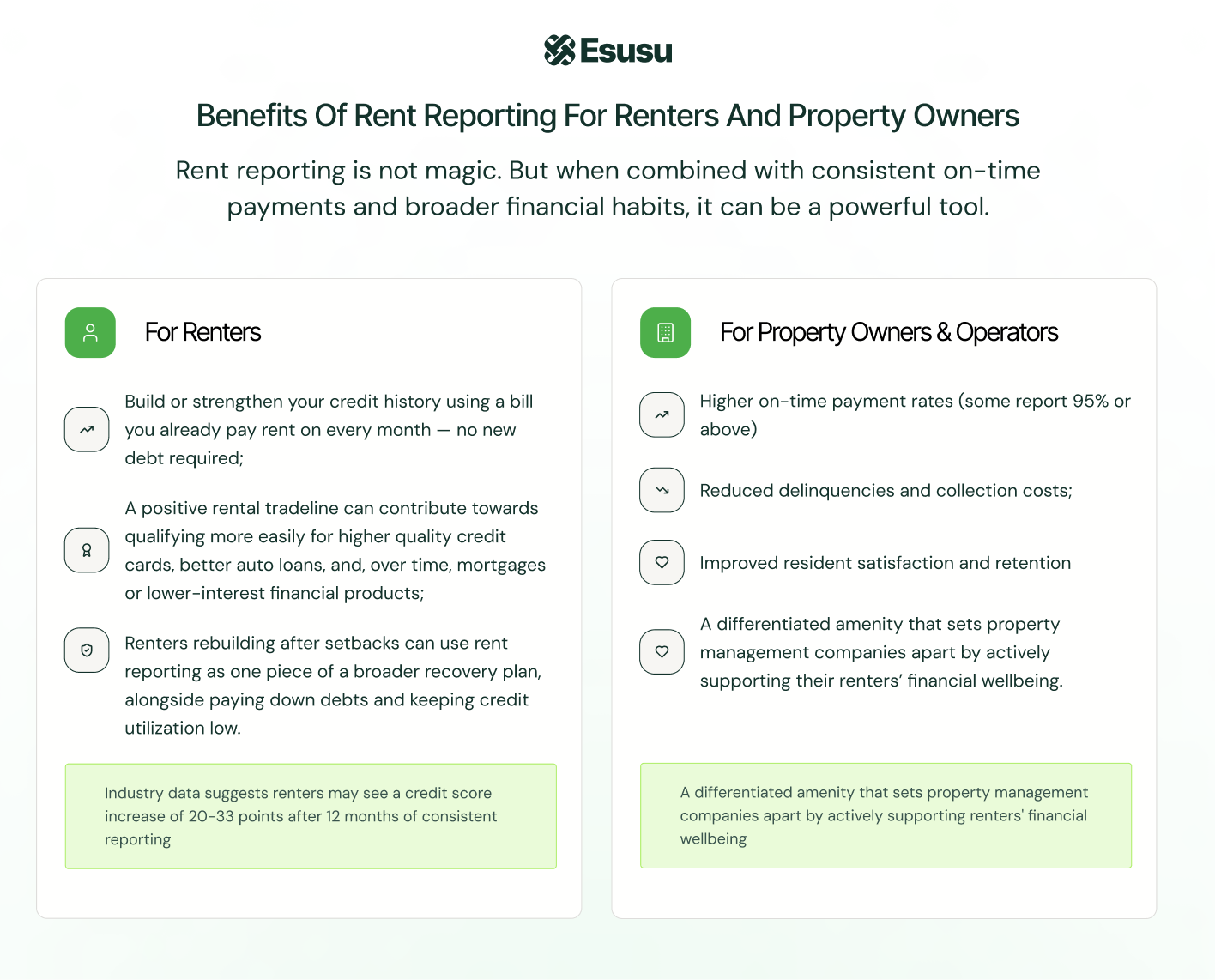

How Esusu Approaches Rent Reporting and Fees

Esusu is a U.S.-based fintech platform dedicated to financial inclusion — meaning we strive to ensure everyone in the U.S., regardless of background, location, race, education, or other factors, has access to tools that improve their financial wellbeing.

While we do partner with property owners, operators, housing providers, and many other businesses, to report on-time rent payments to all three major credit bureaus - Equifax, Experian, and TransUnion - we also offer rent reporting services directly to independent renters via our Esusu app without requiring landlord involvement.

Our resident-first philosophy means helping renters — especially those who have been historically excluded from traditional credit — build your credit using the rent you already pay. We prioritize clear communication and non-predatory practices.

Beyond rent reporting, Esusu also offers related tools for property partners:

- Analytics dashboard to track portfolio and property-level impacts;

- Identity verification, fraud prevention, and income verification for tenant screening process;

- Flexible rent payment solutions.

And for residents:

- Financial coaching to improve credit scores, increase savings, and decrease debt;

- A renter marketplace to connect with curated financial products and savings;

- Rent relief support (available at select Esusu contracted properties);

- Flexible, split rent payments to improve renter cash flow.

Property owners and operators can schedule a demo to discuss pricing and implementation. Renters can sign up independently of their landlord by simply downloading the Esusu app and creating an account. If your property is already enrolled in our rent reporting services, the app will confirm that via your rental address.

Practical Tips for Renters Before You Sign Up

Before enrolling in any rent reporting service, use this checklist when talking to your landlord, property manager, or provider:

Questions to ask:

- Which credit bureaus do you report to?

Coverage of all three — Equifax, Experian, and TransUnion — can provide broader benefits then just reporting to a single bureau. - Do you report only on-time payments, or also late or missed payments?

If so, when is a payment considered late and when does it get reported? - What are the rent reporting fees, and are there any hidden costs?

Get clear, written information: who pays, how much per month or year, whether there’s a separate charge for reporting past payments, as well as any setup fees. - Can I stop rent reporting later?

How do I cancel, are there any penalties, and what happens to my existing rental tradeline if I move or end my lease? (with Esusu, you can transfer your service to any rental) - How is my personal data protected?

Is information shared beyond the credit bureaus? Does the service comply with U.S. privacy and consumer protection laws?

Finally, monitor your credit reports at least once a year using AnnualCreditReport.com (one free report per year, per bureau) to confirm that your rental payment history is appearing correctly — and dispute any errors promptly.

Conclusion: Using Rent Reporting as a Tool for Long-Term Financial Health

So, what is rent reporting? It’s a way to turn a major monthly expense, rent, into a potential asset for building positive credit history.

When rent reporting fees are reasonable and transparent, rent reporting can be an equitable, low-friction way to enter or strengthen your place in the credit system — without taking on new debt or high-risk credit accounts.

If you’re a renter, you can download the Esusu app today to verify whether your rental community offers rent reporting for free through a partnership with Esusu by entering your rental address. If your property isn’t partnered with Esusu, don’t worry — you can simply sign up directly within the app and start building your credit history right away.

Remember: small, consistent steps — like paying rent on time and making informed choices about services and fees — can add up to meaningful progress toward long-term financial stability. Being financially responsible with your rent is already something you do; now it can work for your future.

For property owners and operators, banks, employers, financial or government institutions: Schedule a demo with Esusu to explore how rent reporting and financial health tools can support both your communities and your business goals.

FAQ

*Based on active renters at active properties from enrollment through Q4 2025. Average credit score increase calculated by comparing enrollment credit score to latest available credit score as of Q4 2025, treating renters with no credit score at enrollment as having a score of zero. Esusu only reports on-time rent payments and does not report missed or late rent payments to the credit bureaus. Using Esusu rent reporting services does not guarantee an increase in credit scores or approval for any credit product, as scores are determined by credit agencies using multiple factors including payment history on other accounts, credit utilization rates, and other variables. Individual results vary and are not guaranteed.