.svg)

The 4 Million Homes Gap: How Your Monthly Rent and Credit Scores Could Be the Secret Key to 2026 Homeownership

Let’s be real: If there were an Olympic sport for “Writing Checks That Make Us Cry,” paying rent would take the gold every single time. For most of us, rent isn’t just a bill; it’s a giant, monthly mountain we climb.

Yet, for decades, the credit world treated this mountain like a molehill—or worse, like it didn’t exist at all. You could pay $2,000 a month for ten years straight without a single late payment, and the credit bureaus would just shrug. But miss one $15 payment on a credit card you forgot you had? Believe it or not, straight to jail (metaphorically speaking).

We decided enough was enough. We went down the Reddit rabbit hole of r/CRedit to see what real people were saying. The consensus? A lot of skepticism, a dash of hope, and a whole lot of confusion.

Part of this confusion comes from the existence of different credit scores produced by various scoring models, like FICO and VantageScore, which can lead to different results for the same person. So, we rolled up our sleeves, grabbed our data goggles, and partnered with VantageScore to get to the bottom of it.

The result? A landmark study of 600,000 anonymized renters to prove your rent isn’t just an expense—it’s a financial power move waiting to happen.

The Great Credit Disconnect: What Is VantageScore Anyway?

Before we get into the juicy data (yes, data can be juicy), let’s clear up the alphabet soup of credit scoring.

When you check your credit score—whether it’s through your banking app, Credit Karma, or directly with a credit bureau—that three-digit number is generated by one of two major players: FICO or VantageScore. The FICO score is the most commonly used credit score by lenders.

Think of them like Coke and Pepsi. They both want to quench your “creditworthiness” thirst, but their recipes are slightly different. VantageScore was developed jointly by the big three bureaus—Equifax, Experian, and TransUnion. It’s the modern, tech-savvy cousin of the credit world. It uses machine learning to look at who you are as a human being, rather than just a snapshot of your debt today. Both FICO and VantageScore consider common factors such as payment history, amounts owed, and length of credit history, but may weigh these factors differently and may also include other factors like rent and utility payments.

For our research, we fed our data into the VantageScore 4.0 model. While older models focus on your current balances, 4.0 looks at your behavior over time. It incorporates alternative data: things like utilities and, most importantly, rental history. Credit scores are calculated using algorithms that analyze your credit report, focusing on payment history, debt levels, and credit age.

This model is specifically designed to help people with thin files (aka people who aren’t drowning in credit card debt but have a solid history of paying their bills). It’s not just about identifying risk; it’s about identifying reliability.

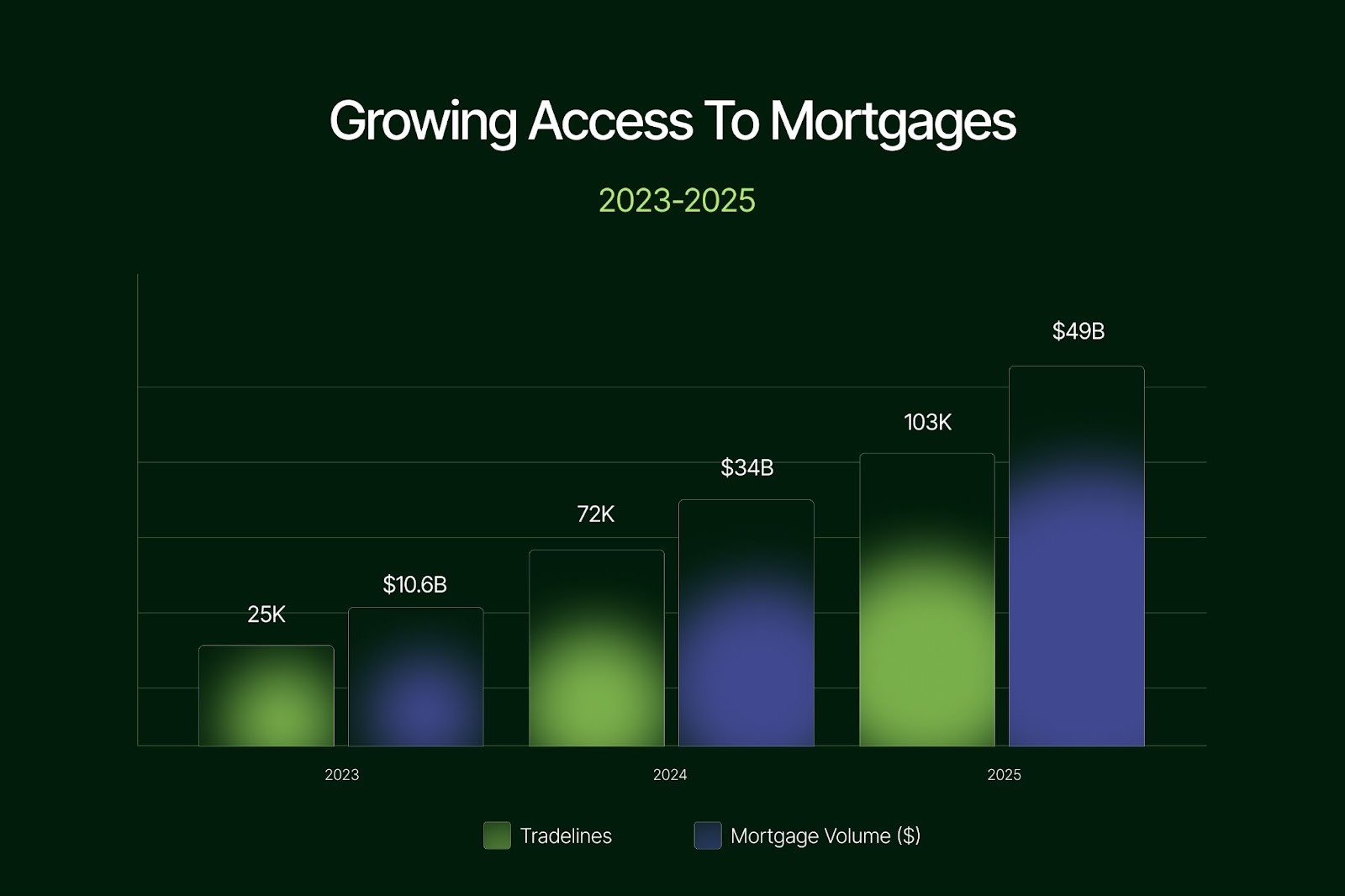

The Proof: 4 Million Invisible Homeowners

The findings of our study were, frankly, undeniable. By simply inviting positive rental history to the credit party, the math changed overnight (read the full report here).

The Headline: By incorporating rent reporting into VantageScore 4.0, 4 million additional Americans could become mortgage-eligible almost instantly. Lenders use credit scores to help decide whether to give you credit and what the terms will be, and higher credit scores signify lower risk, leading to better loan approval rates and interest rates.

Let that sink in. That is 4 million people who are currently paying their landlords’ mortgages who could be paying their own.

Breaking Down the Data

Our study highlighted three key pillars that prove rent reporting isn’t just “fluff”—it’s hard science:

- A Better Crystal Ball: Adding rental history to VantageScore 4.0 actually improves the model’s predictive performance. It identifies up to 11% more defaults and provides a 3.7% predictive lift. In plain English? Rent data makes the score more accurate, not less.

- The “Same-Risk” Reality: Renters who hit a score of 620 or higher because of their rent data perform exactly like homeowners with the same score. They aren’t “riskier”—they were just “hidden.”

- The Near-Prime Powerhouse: This isn’t a “subprime” group. These are “near-prime” and “prime” renters who have been demonstrating financial discipline for years. They were just trapped in a credit limbo where their largest expense didn’t count toward their future.

Why 2026 is Your Year of the "Power Move"

If you’re reading this in 2026, you are standing at the edge of a massive shift in the housing market. For years, the dream of homeownership felt like it was behind a "FICO-only" velvet rope. Not anymore.

In a move that we can only describe as "long overdue," FHFA Director Bill Pulte issued a landmark directive in July 2025. He officially ordered Fannie Mae and Freddie Mac to ditch the legacy models and adopt VantageScore 4.0.

Why does this matter to you? Because for the first time in history, the people who buy your mortgages (Fannie and Freddie) are required to use a model that understands the value of your rent payments. By December 2025, even FICO jumped on the bandwagon with their 10T model, which also factors in rent.

The wall has been torn down. Your rental tradeline is now a legitimate, heavy-hitting asset in the eyes of mortgage lenders.

The Zillow Prediction for 2026

Adding fuel to the fire, Zillow predicts that by the end of 2026, the typical home should be affordable in 20 major U.S. markets. We are looking at a Trifecta of Progress:

- Slow-growing home prices (finally, the brakes are on).

- Falling mortgage rates (cheaper money).

- Rising incomes (more fuel for your fire).

If buying your first home is on your 2026 vision board, a strong credit score—bolstered by your consistent rent reporting—is the single biggest unlock you can have.

Stop Paying Rent for "Nothing"

In the past, rent was a sunken cost. You paid it, you stayed dry, you moved on. But in 2026, failing to report your rent is like leaving a $2,000 stack of cash on the sidewalk every month.

You’ve already done the hard work. You’ve made the payments. You’ve balanced the budget. Now, it’s time to make sure the Big Three bureaus know about it.

The Bottom Line

The 4 Million Homes Gap is closing, and it’s closing because data is finally catching up to reality. You are more than a credit card balance. You are a consistent, reliable, and "homeownership-ready" individual. It’s time your credit score reflected that.

Ready to turn your rent into a credit-building machine? Sign up for myEsusu to get started today.