Financial stress contributes to late payments and turnover. Esusu turns on-time rent into a full financial wellness ecosystem, credit building, loyalty, and stronger portfolio performance.

Resident insightsReal-time portfolio and resident impact data

Rent reportingReports to all 3 major credit bureaus (Experian, Equifax, TransUnion)

Credit Building & Financial WellnessAccess to Financial coaching, education, and more

Flexible rent paymentsRent payment solutions that help prevent missed payments and displacement

Manual review often misses fake pay stubs and stolen IDs, leading to bad debt. Esusu Identity Services quickly flags tampered documents and fraudulent applicants, protecting NOI for as little as $0.99/unit.

Income verificationCatch edited or falsified pay stubs and bank statements

Identity verificationDetect fake or stolen IDs in real time

SSN verificationSpot synthetic identities and “CPNs” missed by credit checks

Economic Insights

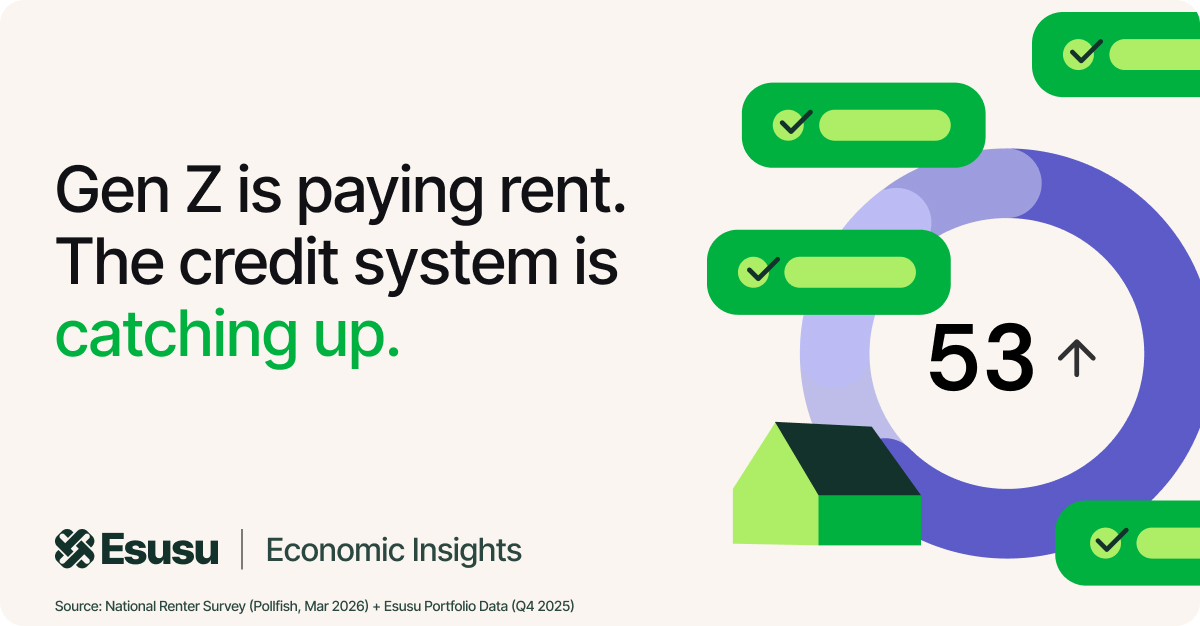

Gen Z Is Paying Rent. The Credit System Is Just Starting to Notice.

Gen Z is doing everything we tell young adults to do.

They’re paying rent. They’re budgeting. They’re trying to build credit. They want to buy homes.

But new data points to an uncomfortable reality: the credit system hasn’t kept up with the behavior that defines modern renting.

Today, we’re releasing new findings from a national survey of U.S. renters aged 18-80, revealing how renters, especially Gen Z, view credit, rent reporting, and the path to homeownership. The survey data comes alongside the launch of the Rent Worth Gap Report, which analyzes outcomes from 2.3 million renters, a subset of those enrolled in Esusu-powered reporting programs. You can read the full Rent Worth Gap Report here.

Gen Z Renters Are Paying at Mortgage Scale, Without Mortgage Credit

The survey shows that 30% of Gen Z renters say their rent is higher than a typical mortgage in their area. And the emotional impact is clear:

Over 60% of Gen Z renters say they feel financially “treading water” by paying rent each month.

60% say Gen Z faces the most difficult path to homeownership.

They are paying large, recurring housing bills, often comparable to mortgage payments, without building equity and, historically, without receiving housing-based credit recognition.

That gap matters even more as newer scoring models like VantageScore 4.0 expand how reported rent payments can factor into credit visibility for renters.

The broader Rent Worth Gap Report reinforces the scale. Among renters enrolled in Esusu-powered programs, the average monthly rent is $1,929, or more than $23,000 per year. Over a decade, that approaches a quarter of a million dollars in housing payments.

Esusu Calculator

Esusu

Your Rent is Worth More.

Financial Identity

Stop paying "Quiet Rent."

You wouldn't pay for a car for 5 years without building credit. Why do it with your home?

Impact Calculator

Official Report

Estimated Total Paid

$0

Verified History0 Months

Payment StatusVerified

ESTIMATED IMPACT: +53 POINTS*

*Based on average credit score increases for Esusu members.

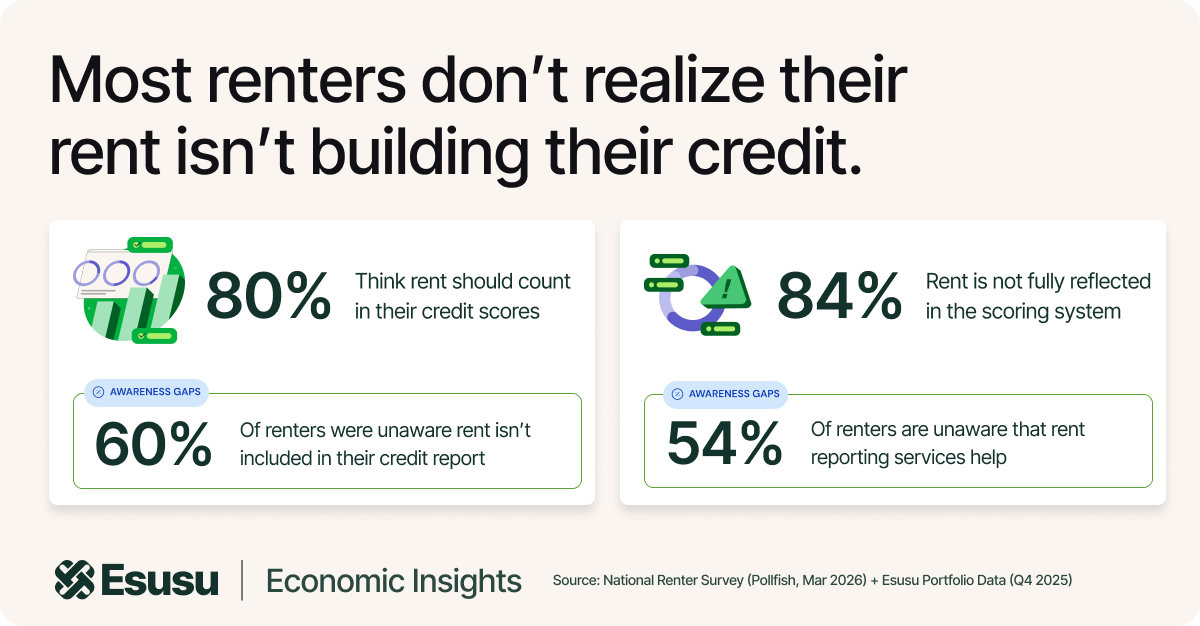

Renters Want Rent to Count — But Many Don’t Know It Doesn’t

Renters overwhelmingly believe rent should be treated like a mortgage in credit scoring:

80% say rent should be considered in credit scoring, similar to mortgage payments.

84% say rent payments are not fully reflected in the credit scoring system.

But awareness gaps are still holding renters back, especially Gen Z:

Nearly 60% of Gen Z renters are not aware that rent payments are not automatically included in their credit score.

54% of Gen Z did not know that there are voluntary services that report on-time rent payments to help build credit.

77% say automatic inclusion of on-time rent would make them feel more financially prepared to pursue homeownership.

This matters because Gen Z is earlier in their credit journey. Older renters may have longer credit histories built through auto loans, credit cards, or prior mortgages. Gen Z renters often do not. When their largest recurring payment is not included, the impact on their credit profile is proportionally larger.

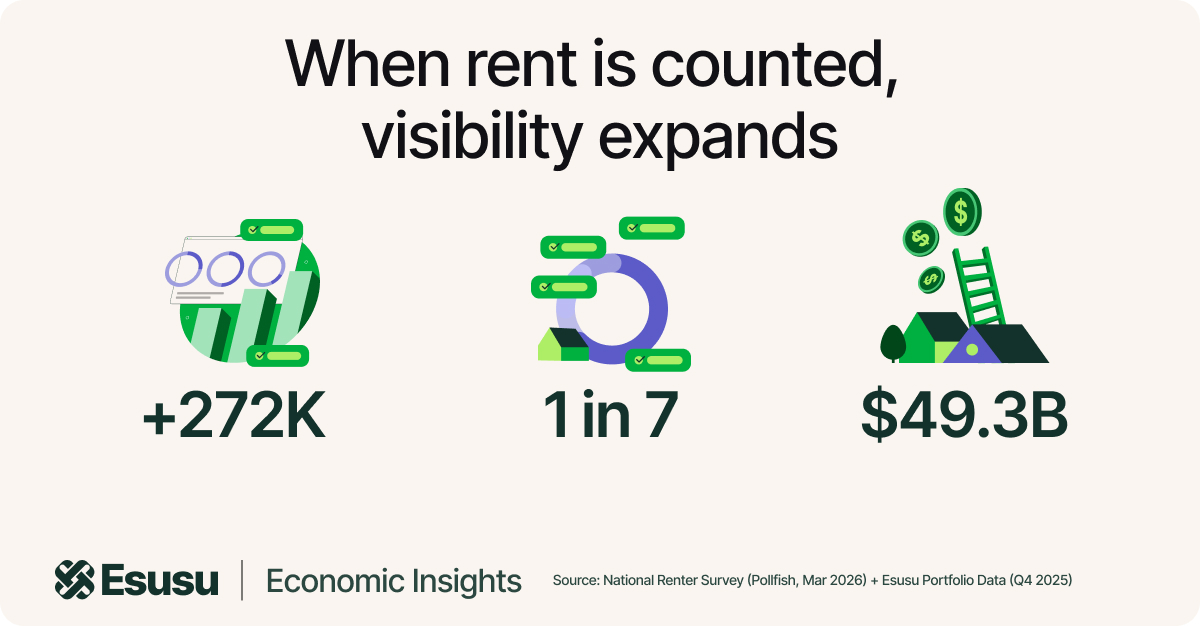

When Rent Is Counted, Credit Visibility Expands

The Rent Worth Gap Report shows what happens when rent transitions from invisible to reported.

Among 2.3 million of the renters enrolled in Esusu-powered rent reporting:

More than 272,000 previously credit-invisible renters became scorable

1 in 7 renters who began below a 660 credit score crossed into mortgage-eligible territory

Renters unlocked $77 billion in credit activity, including $49.3 billion in mortgages

These outcomes span age groups — but they are especially meaningful for renters who are early in building credit, and for a generation paying housing costs that increasingly resemble mortgage payments.

The Bottom Line

The Rent Worth Gap describes the growing disconnect between housing payments made and housing payments formally recognized in credit frameworks. Closing that gap isn’t about taking on new debt. It’s about counting the payments already being made and building a credit system that reflects the American housing system today. Read the full Rent Worth Gap report here.

Methodology

This report combines two data sources:

Esusu Portfolio Data: Aggregated, anonymized outcomes from more than 2.3 million of the renters enrolled in Esusu-powered rent reporting programs across participating properties through Q4 2025. This dataset includes credit invisibility rates, credit score movement, and observed credit origination outcomes.

National Renter Survey (Pollfish, March 2026): A nationally representative survey of 2,000 U.S. renters assessing awareness of rent reporting, perceptions of credit fairness, homeownership readiness, and adoption drivers.

“Credit invisible” refers to renters without sufficient credit history to generate a score prior to enrollment. “Mortgage-eligible” refers to renters whose scores moved above 660 after reporting. National scaling estimates are illustrative and based on observed per-capita outcomes within the Esusu dataset.

.svg)

.jpg)